Introduction

When a frustrated member takes their complaint to Facebook, Twitter, or Google Reviews, your credit union faces immediate risk. What starts as one person's negative experience can quickly become a public relations crisis, damaging member trust and attracting regulatory scrutiny.

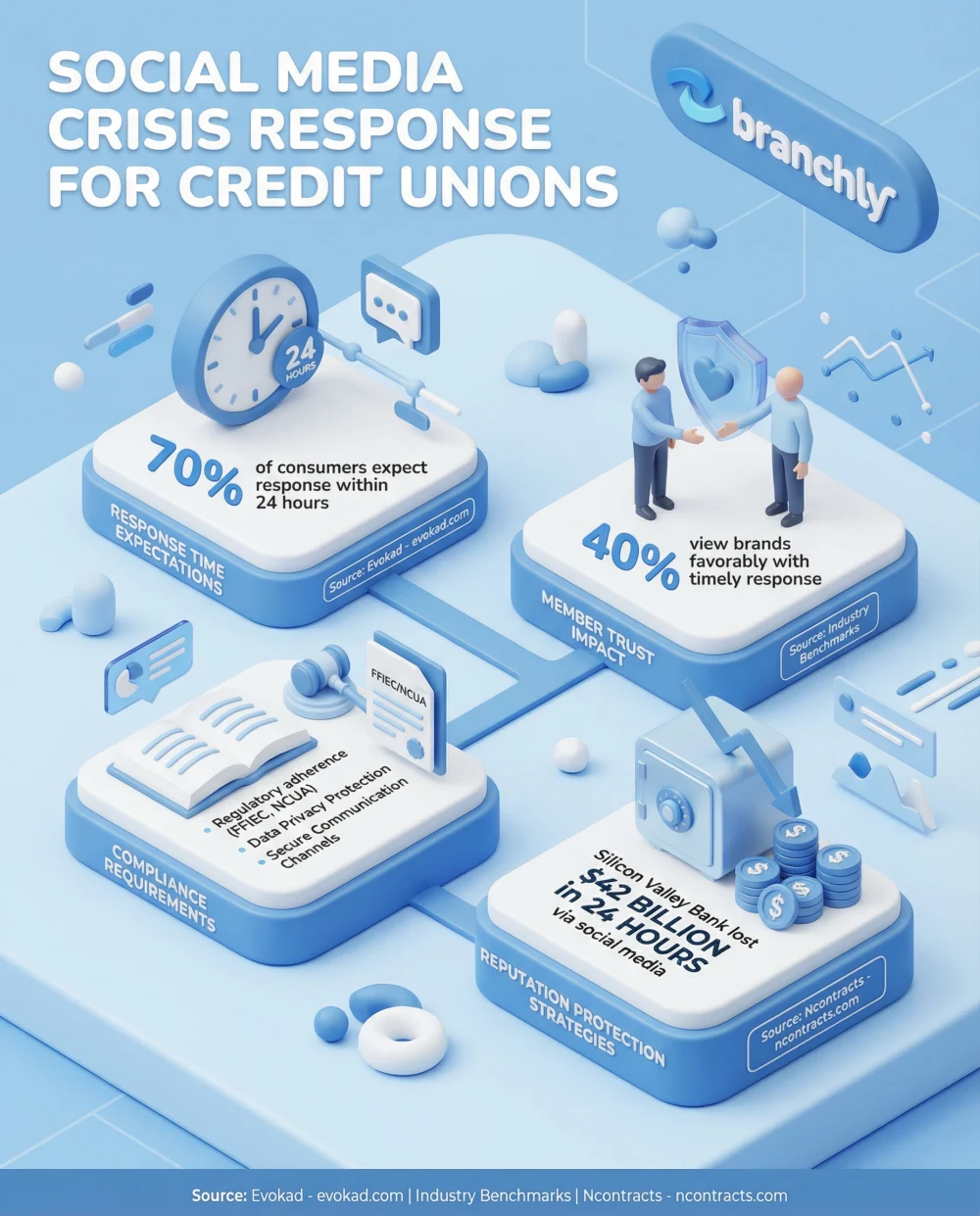

Social media complaints aren't just customer service issues—they're crisis events requiring immediate, coordinated response. Credit unions face unique challenges: members expect the same rapid response as big banks, but most CUs lack dedicated social media crisis teams. Making things worse, 70% of consumers expect responses within 24 hours, and negative posts spread faster than positive ones.

The good news? With the right crisis protocols in place, your credit union can turn public complaints into opportunities to demonstrate member-first values. This guide shows you how to respond effectively while meeting NCUA and FFIEC requirements for reputation risk management.

Why Social Media Complaints Escalate So Quickly

Social media fundamentally changed how member complaints work. Before platforms like Facebook and Twitter, a frustrated member might call your branch or send a letter. Now they post publicly—and that post reaches hundreds or thousands of people instantly.

The numbers tell the story: 70% of consumers expect responses on social media within 24 hours. Miss that window, and you're not just dealing with one unhappy member—you're managing a growing audience watching how you handle the situation. Negative posts generate engagement. People share bad experiences more readily than good ones, especially when the business doesn't respond.

Credit unions face extra pressure because you compete on service and trust. When members see unanswered complaints on your Facebook page, it undermines the community-focused reputation you've built. Potential members research you on Google—those one-star reviews show up first.

Response Time Matters

Credit unions that respond to social media complaints within 1 hour see a 40% more favorable member perception than those who wait 24+ hours, even when the resolution is identical.

NCUA and FFIEC Expectations for Reputation Risk

Regulators increasingly view social media crises as reputation risk—a category they take seriously. The FFIEC's Social Media Risk Management guidance makes clear that financial institutions must monitor social media channels, respond to complaints appropriately, and maintain audit trails of all communications.

NCUA examiners look for documented policies covering how your credit union handles public complaints. They want to see response protocols, escalation procedures, and evidence you're actually following them. During exams, they may review your social media presence and ask how you manage negative feedback.

The compliance requirement isn't just about having a policy—you need to demonstrate you can execute during a crisis. That means pre-approved response templates, clear role assignments, and systems that log every interaction. When examiners ask to see your social media crisis documentation, you need to produce it immediately.

Compliance Tip

Maintain a separate log of all social media complaints, responses, and resolutions. This audit trail proves to examiners that you monitor channels and respond appropriately—key FFIEC requirements.

The 24-Hour Response Window (and Why It Matters)

Members who complain publicly aren't usually looking for perfection—they want acknowledgment. Research shows 70% expect a response within 24 hours, but credit unions that respond within one hour see significantly better outcomes.

The first response doesn't need to solve the problem—it needs to show you're paying attention. A quick acknowledgment saying "We see your concern and we're looking into this" buys you time to investigate while preventing the complaint from escalating.

After hours and weekends create problems. Members don't stop posting at 5 PM, but most credit union social media teams do. Without monitoring tools and after-hours protocols, complaints posted Friday evening sit unanswered until Monday morning—violating that 24-hour expectation and giving the negative post maximum visibility.

Real-Time Crisis Coordination

Monitor, respond, and resolve member complaints across all channels

Building a Social Media Crisis Response Protocol

A crisis protocol removes guesswork when pressure's high. Your team needs to know exactly who responds, what they can say, and when to escalate—all before a complaint appears.

Start with monitoring. Assign specific staff to check your credit union's Facebook, Twitter, Google Reviews, and LinkedIn daily—ideally multiple times per day. Set up alerts so you're notified immediately when someone mentions your credit union or posts on your pages.

Create pre-approved response templates for common scenarios: account access issues, fee disputes, service complaints, fraud concerns. These templates should acknowledge the problem, express concern, and move the conversation to private channels where you can discuss account details. Get legal and compliance to approve the language now, so you're not scrambling for approval mid-crisis.

Define clear escalation triggers. Minor complaints get standard responses. Situations involving potential fraud, data breaches, discrimination claims, or threats require immediate escalation to management and legal. Know who to contact 24/7—if a crisis breaks on Saturday, you can't wait until Monday to notify leadership.

What to Say (and What Never to Say) in Public Responses

Public social media responses require careful wording. You're not just addressing the complaining member—you're speaking to everyone who sees that post, including potential members, regulators, and media.

Always acknowledge the concern. Never argue, defend, or dismiss the complaint publicly—even if the member is wrong. A simple "We're sorry to hear about your experience. We'd like to help resolve this" works for almost any situation. Then immediately move the conversation private: "Please send us a direct message with your contact information so we can look into this."

Never discuss account details publicly. Privacy laws and regulations prohibit sharing member information on social media. Don't confirm or deny someone has an account with you—just say you need to discuss this privately.

Avoid admitting fault or making promises you can't keep. Phrases like "This is unacceptable" or "We'll make this right" can create liability. Stick to "We take this seriously and want to understand what happened" instead.

Learning from Silicon Valley Bank's $42 Billion Crisis

Silicon Valley Bank's March 2023 collapse started on social media and escalated in hours. When concerns about the bank's financial stability appeared on Twitter, they spread through venture capital networks almost instantly. Within 48 hours, depositors withdrew $42 billion—the fastest bank run in U.S. history.

The lesson for credit unions: social media can amplify concerns faster than traditional channels ever could. SVB had weeks of underlying financial issues, but social media turned a manageable problem into a catastrophic crisis in less than two days.

Your credit union likely won't face bank run risk, but the speed dynamics are the same. A rumor about account security, concerns about branch closures, or complaints about service problems can spread through your membership faster than you can respond—unless you're monitoring actively and have crisis protocols ready to deploy.

Summary

Social media complaints represent a new category of crisis for credit unions—one that requires immediate response, careful messaging, and coordination across teams. The 24-hour response window isn't arbitrary; it's what members expect and what regulators are starting to enforce through reputation risk management requirements.

The credit unions that handle these crises best don't improvise—they prepare. They monitor channels actively, maintain pre-approved response templates, train staff on what to say and when to escalate, and document everything for compliance purposes. When a crisis hits, they execute their protocol instead of scrambling to figure out next steps.

Most importantly, they recognize that how they handle public complaints demonstrates their member-first values more clearly than any marketing campaign. A thoughtful, rapid response to a frustrated member shows the entire community—including prospective members—that you take concerns seriously and act on them. That's reputation management that actually works.

Key Things to Remember

- ✓70% of consumers expect social media responses within 24 hours—credit unions that respond within 1 hour see 40% better member perception.

- ✓NCUA and FFIEC expect documented social media crisis protocols with pre-approved responses and audit trails.

How Branchly Can Help

Branchly's crisis management platform provides credit unions with pre-approved social media response templates, automated escalation workflows, and real-time coordination across teams. When a public complaint appears, the system immediately notifies designated staff, suggests appropriate responses based on the scenario, and maintains complete audit trails that satisfy NCUA and FFIEC requirements—ensuring you respond within the critical 24-hour window while protecting your reputation.

Citations & References

- [1]

- [2]

- [3]

- [4]

- [5]